What happened if you paid 20x sales for MSFT at IPO? What happened if you assumed AMZN could hit WMT’s margins?

Before I begin, I have a confession to make. Despite running a “value” fund, I am actually an AMZN shareholder. Since 2013, I have owned exactly one share. The purchase served several purposes – for instance, a reminder never to short it – but I primarily bought because I saw the competitive advantages and growth opportunities. At the time, I was a consumer analyst at a hedge fund and saw the shift to e-commerce and the challenges brick-and-mortar retailers faced to adapt. AMZN was clearly winning, and the gap was only growing harder to bridge. In my mind, the question was not whether AMZN was the type of investment I wanted to make but at what price. The same can be said for MSFT, the other subject of this post. While MSFT might have been a bit further in its growth curve, it doesn’t take a genius to realize a 40-year monopoly on PC operating systems and a ubiquitous suite of office work staples make good barriers to entry. Sadly, I never owned either in size and since my AMZN purchase in Fall 2013, AMZN and MSFT revenues have grown 526% and 126%, respectively, which compares to the S&P 500 at 40% – software is indeed eating the world. However, there is a small catch: despite AMZN considerable outgrowth, MSFT shares are the slight outperformer, rallying 958% vs. AMZN’s 933% and the S&P 500’s 176% return. The explanation is that MSFT has experienced significant multiple expansion. In the early 2010s, as current tech bulls may forget, MSFT and many other tech companies traded at below market multiples due to fears surrounding the impact of cloud computing and the shift from desktop to mobile. As MSFT executed and emerged as a leader in cloud computing, its multiple expanded significantly from 10-13x EPS in 2013 to 30-40x today. Which brings me to the point of this post – entry price matters.

In the current tech bull market, there’s a popular belief that growth trumps all and entry price is for “old timers.” There are now dozens of companies trading 20x EV/Sales or more, a level that would have been considered “ridiculous” only a few years ago. Like any popularly held belief, there is some logic and support behind it. The general idea is that if there is enough growth, the long-term compounding of said growth, along with the subtle if unstated belief that superior margins are inevitable, will dwarf any difference in entry price. (This recent, well-written piece is geared towards early-stage investments but lays out the thesis.) Bulls can point to numerous recent success stories of the wisdom of paying up, from Andreessen Horowitz famously breaking the post-Dot Com Silicon Valley paradigm to hedge funds riding a wave of SaaS to market beating returns. While the “old timers” might point to numerous previous periods of tech exuberance ending in crashes, bulls can simply retort, “I’m just going to hold – just look at MSFT and AMZN!”

So, let’s put this strategy to the test. What if instead of looking at recent success, we went back to MSFT’s IPO and applied a 20x sales framework? Surely if bulls are comfortable paying 20x EV/Sales for numerous names currently, they’d be comfortable buying the ultimate winner – the world’s largest company with 42% margins – at IPO. Further, let’s ask if we actually had to pay up to get these amazing returns seen lately. I’ve already established that we could have purchased MSFT at a reasonable price a decade ago, but what about AMZN? Jeff Bezos aggressively reinvested and ran his company at negligible profits for years in pursuit of the dominant position it reached today, but could we have made reasonable margin assumptions and valued it versus peers? Let’s dig in.

MSFT IPOed on March 13, 1986, at a price of $21 per share with roughly 24.7MM shares outstanding, yielding a market cap of $519MM. In MSFT’s fiscal year ending June 1987, the company had revenues of $346MM. Using a 20x multiple, that implies a market cap of $6.9B, 13x its actual IPO price. Compared to MSFT’s current cap of roughly $2.5T, that yields an IRR of 18.0%. Not too shabby. (Yes, I realize MSFT has had a dividend in recent years, but it’s small, difficult to adjust into IRR, and wouldn’t move this math much.) However, let’s put some context around that. During this time, the S&P 500 annualized return was 11.2%. MSFT stock is still a solid outperformer, but humbler than I think most would expect for buying the tech GOAT at IPO. MSFT also experienced a not-so-subtle 16-year “pullback” where one had to maintain their firm belief in MSFT’s inevitable re-emergence as a leader. One would have had to maintain this belief as MSFT repeatedly missed virtually every major tech trend for two decades: the initial growth of the internet, e-commerce, search, consumer electronics, social media, mobile, streaming video, etc. Any weak-handed trading in that stretch could easily have cost a few hundred bps off our IRR.

Now let’s approach this from a portfolio perspective. So far, we are only looking at MSFT, an unquestionable tech winner, but very few investors are proposing to buy exactly one stock. What could our long-term tech portfolio have looked like? The second and third hottest IPOs of 1986 were ORCL and Sun Microsystems. How have they done? ORCL has achieved a 20.1% CAGR since then, but it falls to 13% if you paid 20x sales. Sun Microsystems was eventually acquired by ORCL for a 9.4% CAGR since IPO, but at a sub-1x sales exit multiple and for $5.6B ex-cash. The fourth hottest 1986 IPO? Teknowledge, the era’s leading player in artificial intelligence. It eventually got absorbed into a Pittsburgh industrial. IBM’s CAGR is sub 5%, and it traded nowhere near 20x. This pattern would also hold for tech companies in a later era. If you paid 20x EV/Sales for GOOGL’s IPO, your return would be 20.7%. But you better not have bought Yahoo, Lycos, AOL, Cognos…

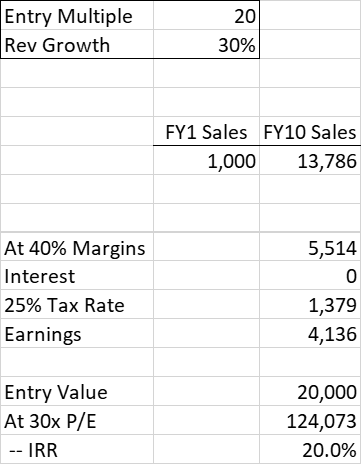

Historically, it’s been exceedingly difficult to pay 20x sales for a portfolio of companies and end up beating the market in the long run. A simple model shows why – you must grow at an outstanding rate for 10+ years and you cannot exit anywhere near a market multiple. Take, for example, a company that grows sales at 30% for 10 years and achieves a 40% operating margin. If we exit at a 30x P/E multiple, or a PEG of 1.0 assuming margins are stable, we achieve a 20.0% IRR:

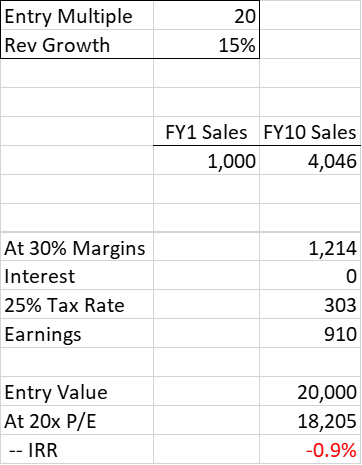

That’s actually very close to MSFT’s return in the 1990s. MSFT’s revenues went from $1.84B in 1991 to $25.3B in 2001, a 29.9% CAGR, and traded ~25-35x EPS in the early 2000s. By buying at 20x EV/Sales, bulls are basically saying, “I am long MSFT-type companies, and only MSFT-type companies, to achieve a 20% IRR.” If a company instead “only” achieves a 15% revenue growth rate, 30% margin, and a 20x P/E at exit, we lose money:

For reference, that’s basically ADBE in the 1990s. Sales grew at roughly an 18% CAGR, achieved 28-33% operating margins, and the stock traded 20-25x in the early 2000s. In my opinion, a strategy where we make 20% IRRs if we only pick MSFT and we lose money if we pick ADBE, in its own right an excellent business, is not a particularly good risk/reward investment framework.

Which brings me back to my central point: entry price matters. If we are going to pick a long-term winning strategy, completely ignoring entry price is unlikely to be a wise decision for anything beyond small, early-stage businesses. So, let’s take AMZN. For years, “value investors” derided AMZN as a nice company that did not make any money. In fairness, AMZN’s lack of GAAP profits or FCF made it difficult to analyze, but could we have used reasonable assumptions and found an entry at reasonable prices?

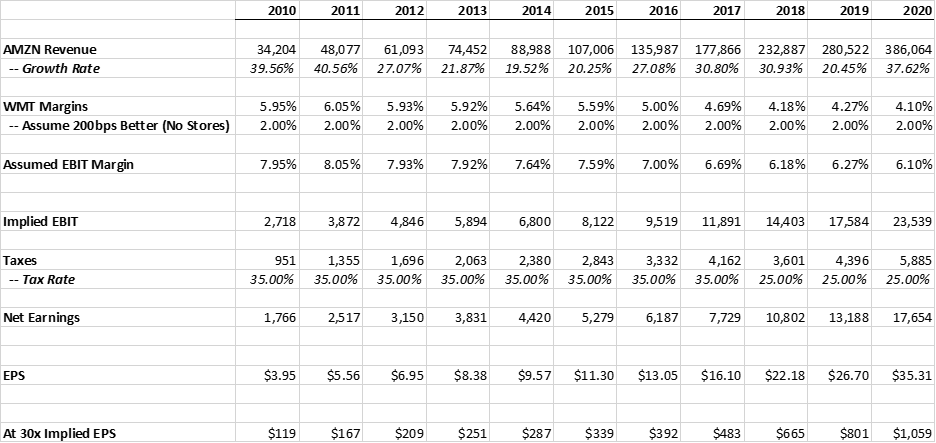

Back when I bought my (massively sized) AMZN investment, I created a general framework to assign AMZN a P/E multiple. At the time, given AMZN’s “everything store” approach, I thought of AMZN as WMT without the stores. I guessed that if it weren’t for all its growth investments, AMZN could at least achieve WMT’s margins plus 200bps. I then backed out taxes for a guess owners’ earnings. My reasoning was simple. Rent is typically 5-15% of sales for a retailer, plus AMZN had significant 3P revenues (EBAY at ~20% margins) and Prime subscriptions which I felt made my assumptions conservative. AWS was relatively small at the time, but I saw the opportunity and figured a business with significant software components could at least achieve WMT’s margins. However, given my concerns on eventual margins – at the time, renting a server seemed pretty commodity to me – I was humorously only willing to buy AWS “for free.” Applied retroactively, here’s the general look of my work:

At the time, growthy retailers typically traded 30x or more EPS (ULTA, WFM, COST) while mature retailers traded closer to 15x (WMT, TGT), so anything sub 30x was a starting place to enter AMZN. So how often did AMZN trade at a “reasonable” multiple using my framework?

If you assumed AMZN could earn at least slightly superior margins to WMT, you could have bought AMZN at 20-30x EPS almost every year from 2001 to 2015. From 2016 onward, the growth of AWS, my previous “freebie,” began to achieve 30% margins and fundamentally reshape the thesis. AMZN might not have been as clear an earnings story as MSFT, but with simple assumptions, AMZN was not some pie-in-the-sky, YOLO revenue story but a modestly expensive yet rapidly growing business.

Conclusion

Stepping back, my general point is that investors are ignoring entry prices at their own peril. 20x Sales at a 30-40% margin and a 25% tax rate is 65-90x earnings, and compression toward even an above market 20-30x multiple leaves you 50-75% in the hole, which is awfully hard to overcome. Further, until recently, most technology stocks traded at reasonable multiples. It’s only in recent memory that multiples have skyrocketed. You still had to pick the correct stocks – IBM and Teknowledge wouldn’t cut it – but you did not have to cross your fingers and hope you exit nowhere near a market multiple.

Finally, in no particular order, some closing thoughts:

- This does not really apply to very early-stage investments. If a company can 1,000x revenues in a decade, multiple is less important, but that is incredibly unlikely with >$1B revenue investments.

- To achieve better than 20% IRRs, you really need to be rotating ideas in addition to and/or instead of picking long-term winners. If MSFT and GOOG at IPO prices reach only mid-20s IRRs, it is incredibly unlikely a portfolio of 20 or 30 stocks held for 10+ year will reach that. Personally, I am still a fundamental investor but prefer to follow the long-term winners and buy them at attractive entry points – earnings misses, macro crises, etc., but I cannot deny that some investors successfully deploy short-term trading strategies that ignore fundamentals.

- For simplicity, I am ignoring taxes but they would have an impact. However, I would argue the largest impact is short-term vs. long-term capital gains, rather than the pre-tax compounding on assets after long-term status is reached. I might elaborate on that later.

- Entry strategy is important, but exit strategy is even bigger. This post only addressed scenarios where we bought companies that emerged as winners, but every investment strategy will encounter losing investments and growth strategies have historically encountered many long-term misses. How that is managed is ultimately a bigger deal than entry price.